When managing inventory, it’s important to understand the differences between cycle vs physical count methods.

1. Inventory Accuracy Problems Start Before the Count

The cycle count vs physical count decision usually becomes urgent after system inventory stops matching what employees can find in the warehouse. At first, the problem may look like a simple counting failure. However, the discrepancy often began much earlier during receiving, putaway, picking, returns, transfers, production, or manual data entry.

For example, a receiver may record 100 units even though only 90 arrived. Meanwhile, a warehouse employee may place the products in the wrong bin. A transfer may leave one facility without being received into another. Similarly, returned goods may remain classified as sellable even though they are damaged or waiting for inspection.

As a result, inventory records gradually drift away from warehouse reality. Purchasing may reorder stock that already exists, while sales teams promise inventory that cannot be located. Warehouse employees then spend time searching, recounting, and escalating shortages. Finance may also struggle to reconcile inventory values during month-end close.

Therefore, the real objective is not simply to count more often. Instead, businesses need a structured inventory-control policy that identifies errors quickly, supports investigation, and improves the process that originally caused the discrepancy.

1.1 Why Inventory Discrepancies Become Business Problems

Inventory accuracy affects nearly every operational department. When quantities are unreliable, purchasing recommendations become less dependable. Likewise, fulfillment teams may allocate stock that does not exist, while finance reports values that later require significant adjustments.

Moreover, inaccurate records weaken forecasting. A company may interpret a stockout as unexpected demand even though the actual cause was an unrecorded transfer. Conversely, the system may show excess inventory because products were damaged, consumed in production, or shipped without proper confirmation.

Consequently, an inventory discrepancy rarely stays inside the warehouse. It can affect customer service, purchasing, cash flow, gross margin, production schedules, and management reporting.

1.2 Why More Counting Does Not Automatically Improve Accuracy

A warehouse can complete hundreds of counts and still operate with unreliable inventory. This often happens when employees adjust quantities without determining why the difference occurred.

For instance, a product may repeatedly appear short in the same warehouse zone. The team may correct the quantity every month. Nevertheless, the issue will continue if the underlying problem is poor putaway, confusing labels, uncontrolled picking, or an incorrect unit of measure.

A strong inventory-control program should therefore combine four activities:

- Physical verification

- Variance investigation

- Controlled adjustment

- Root-cause correction

Without the final step, counting only resets the balance temporarily. Eventually, the same discrepancy returns.

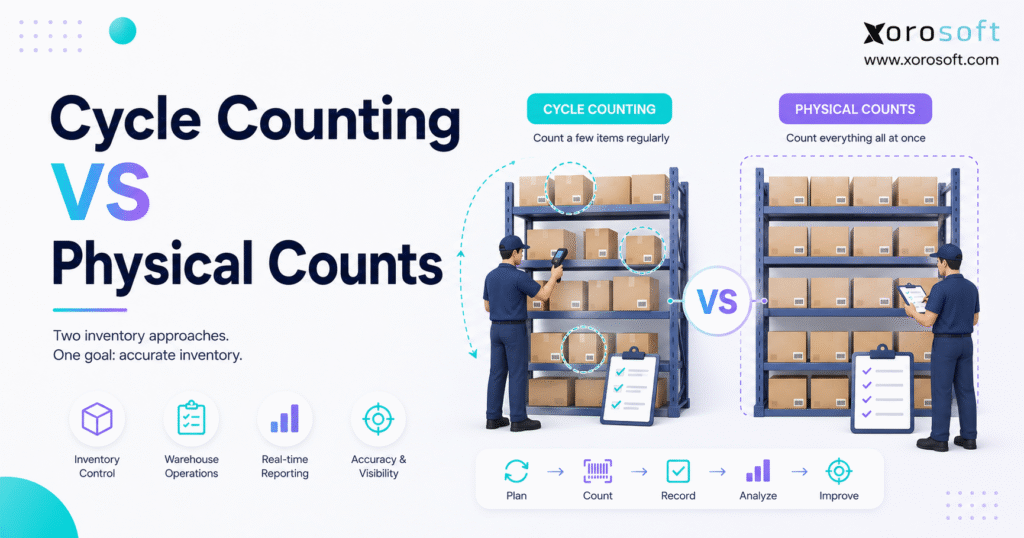

2. Cycle Count vs Physical Count: Understanding the Two Methods

Although both methods compare system inventory with actual stock, they operate differently. In particular, they differ in scope, frequency, labor requirements, disruption, and how quickly they expose process failures.

2.1 What Is Cycle Counting?

Cycle counting is the recurring process of counting selected products, bins, warehouse zones, or inventory classes rather than counting the entire facility at once.

For example, a company may count high-value products every week, fast-moving products every month, and stable low-risk products every quarter. As a result, inventory verification becomes part of normal warehouse operations instead of one large annual event.

Companies may prioritize cycle counts based on:

- Product value

- Transaction velocity

- Variance history

- Customer importance

- Shelf life

- Theft or damage exposure

- Lot or serial requirements

- Production impact

- Warehouse location

- Return frequency

After employees complete the count, the physical result is compared with the system quantity. If the difference exceeds an approved tolerance, the team should recount, investigate, document the cause, and approve the adjustment.

2.2 What Is a Physical Inventory Count?

A physical inventory count verifies every item within a defined scope at a specific point in time. The scope may include the entire company, one warehouse, one store, or one selected product category.

Businesses often conduct a full count:

- At the end of a financial period

- Before an audit

- During a system migration

- After a warehouse move

- Following an acquisition

- When existing balances are unreliable

- Before launching a formal cycle counting program

Unlike cycle counting, a physical inventory count concentrates most of the work into one event. Therefore, preparation, transaction control, staffing, recounting, and reconciliation become especially important.

2.3 What Both Inventory Counting Methods Have in Common

Both approaches require reliable item records, clear warehouse locations, trained counters, defined ownership, tolerance rules, and controlled adjustments.

Additionally, both methods can fail when inventory continues moving without proper transaction controls. For example, an employee may count a product while another employee is picking, receiving, or transferring the same stock. Consequently, even a correct physical count can appear wrong when the timing of system activity is unclear.

The main difference is not whether employees physically count inventory. They do so in both methods. Instead, the difference is whether the business verifies selected inventory continuously or verifies the full defined scope during one event.

3. Cycle Count vs Physical Count: Direct Operational Comparison

The clearest way to evaluate cycle count vs physical count is to compare how each method affects warehouse operations, labor, accuracy, and financial control.

| Comparison factor | Cycle counting | Physical inventory count |

|---|---|---|

| Scope | Selected SKUs, bins, or locations | All inventory within the defined scope |

| Frequency | Daily, weekly, monthly, or quarterly | Annual, periodic, or event-driven |

| Labor model | Distributed throughout the year | Concentrated around one event |

| Warehouse disruption | Usually limited | Often significant |

| Error detection | Continuous | Point-in-time |

| Root-cause investigation | Easier while transactions are recent | Harder when errors accumulated |

| Best fit | Active and complex operations | Complete validation or simpler operations |

| Technology requirements | Benefits from ERP, WMS, and scanners | Can use sheets, tags, scanners, or software |

3.1 Inventory Count Scope and Frequency

Cycle counting focuses on manageable groups of inventory. For example, employees may count one warehouse zone today, high-value products tomorrow, and frequently adjusted SKUs later in the week.

Consequently, the business verifies inventory gradually without stopping every operation at once. Over time, the complete inventory population receives coverage according to a defined schedule.

A physical count follows the opposite model. It verifies all inventory within the selected scope during a defined period. Therefore, the company receives a complete point-in-time snapshot. However, that snapshot begins aging as soon as normal transactions resume.

3.2 Labor Requirements and Warehouse Disruption

Cycle counting spreads labor throughout the year. This generally makes the work easier to absorb within daily operations. Nevertheless, the method requires consistency because missed tasks can quickly reduce inventory coverage.

In contrast, a physical count concentrates labor into a shorter period. The company may require overtime, temporary employees, weekend work, restricted receiving, delayed fulfillment, or a complete warehouse shutdown.

Therefore, cost should not be evaluated only through counting wages. Businesses should also consider:

- Delayed shipments

- Lost warehouse capacity

- Overtime

- Temporary labor

- Recounting time

- Reconciliation work

- Customer-service impact

- Production interruptions

3.3 Inventory Accuracy and Error Detection

Cycle counting identifies discrepancies more frequently. As a result, the team can investigate recent receipts, picks, transfers, returns, or production orders while the supporting details remain available.

A full physical count may identify more discrepancies at one time. However, a difference discovered months after it occurred can be difficult to explain. The team may know that the inventory balance is wrong without knowing which process created the error.

Therefore, cycle counting often provides stronger root-cause visibility, while physical counting provides broader point-in-time coverage.

3.4 Audit and Accounting Considerations

A physical inventory count can support period-end verification because it creates a broad record of stock on hand. Meanwhile, a mature cycle count program can provide evidence of continuous inventory control.

However, businesses should not assume that cycle counting automatically removes every financial, lender, regulatory, or audit requirement. Instead, finance leaders should align the counting policy with accounting procedures, internal controls, and professional guidance.

4. Cycle Count vs Physical Count: Benefits and Limitations

The cycle count vs physical count comparison becomes more useful when teams understand what each method does well and where it can fail.

4.1 Advantages of Cycle Counting

The biggest advantage is earlier detection. A discrepancy identified within days is generally easier to investigate than one discovered several months later.

Moreover, cycle counting can reveal patterns. Repeated differences may involve:

- One warehouse zone

- One product family

- One shift

- One employee process

- One unit of measure

- One transaction type

- One integration

- One supplier

Because the same areas are reviewed repeatedly, managers can determine whether corrective action has worked.

Cycle counting also reduces operational disruption. Instead of closing the entire facility, teams can count selected locations while other warehouse areas continue operating.

Additionally, the method turns inventory accuracy into an ongoing management responsibility rather than an annual project. Consequently, leaders can review completion rates, variance values, and recurring causes throughout the year.

4.2 Limitations of Cycle Counting

Cycle counting can create false confidence when execution is inconsistent. For example, employees may count only accessible products while avoiding mixed bins, bulk storage, overflow locations, or difficult items.

Similarly, overdue count tasks can accumulate. When that happens, the business may believe that all inventory is being reviewed regularly even though some products have not been verified for months.

The method also depends on strong master data. Duplicate SKUs, incorrect units of measure, unclear bin labels, inactive products, and inconsistent warehouse locations can undermine every count.

Therefore, businesses should track not only how many tasks were completed but also which products, bins, and locations have not been counted.

4.3 Advantages of Physical Inventory Counts

A full physical count provides broad coverage and a clear reset point. It is particularly useful when a business no longer trusts system inventory.

Furthermore, the preparation process can improve warehouse organization. Employees may discover unidentified stock, mixed products, damaged goods, expired inventory, or items stored outside approved locations.

A complete count is also valuable before:

- ERP implementation

- Warehouse relocation

- Ownership change

- Financial audit

- Facility consolidation

- Major process redesign

In these situations, a reliable starting balance is essential.

4.4 Limitations of Physical Inventory Counts

The method can be expensive and disruptive. More importantly, it provides only a point-in-time correction.

Once receiving, picking, transfers, returns, and production restart, new discrepancies can appear immediately. Consequently, businesses that rely only on annual counts often spend most of the year working with declining inventory confidence.

A physical count also concentrates risk. If instructions are unclear or warehouse preparation is poor, the entire count may produce unreliable results.

5. Choosing the Right Cycle Count vs Physical Count Strategy

The correct cycle count vs physical count strategy depends on operational complexity, transaction volume, inventory risk, and the consequences of inaccurate stock.

A small company with thousands of variants and several sales channels may need cycle counting earlier than a larger business with a stable product range. Therefore, revenue and employee count should not be the only decision factors.

5.1 When Cycle Counting Is the Better Fit

Cycle counting generally fits businesses with:

- Large SKU catalogs

- High order volume

- Multiple warehouses

- High-value inventory

- Lot or serial tracking

- Ecommerce and wholesale channels

- Seasonal inventory

- Frequent returns

- Continuous fulfillment

- Manufacturing activity

These businesses need discrepancies identified quickly because inaccurate inventory affects daily decisions.

For example, a wholesaler with three warehouses cannot wait until year-end to discover that one location has been shipping incorrect quantities. Likewise, a Shopify merchant may need frequent verification because inaccurate availability can lead to overselling.

5.2 When a Full Physical Count Is More Appropriate

A physical count may be sufficient for a business with few products, low transaction volume, and one organized location.

Additionally, a complete count is appropriate when the company needs a reliable starting balance before a major change. For example, a business may conduct a full count before implementing ERP, moving warehouses, changing ownership, or rebuilding its inventory-control process.

A physical count may also be necessary when existing records are too unreliable to support an effective cycle count schedule. In that situation, the business should first establish an accurate baseline.

5.3 When a Hybrid Inventory Counting Policy Works Best

Many companies should use both methods.

Cycle counting maintains ongoing control, while periodic physical counts provide broader validation. Therefore, a hybrid policy works well when a business needs continuous accuracy but must also satisfy audit, lender, governance, or operational requirements.

A hybrid policy can also vary by warehouse. For example, a mature facility with strong accuracy may rely heavily on cycle counting. Meanwhile, a newer or less stable warehouse may require more complete verification.

5.4 Inventory Counting Decision Matrix

| Business condition | Cycle counting | Physical count | Hybrid approach |

| Few SKUs and low volume | Optional | Strong fit | Optional |

| Thousands of active SKUs | Strong fit | Supplemental | Strong fit |

| Multiple warehouses | Strong fit | Location-specific | Strong fit |

| High-value inventory | Strong fit | Useful validation | Strong fit |

| Lot or serial tracking | Strong fit | Useful validation | Strong fit |

| Major system change | Helpful afterward | Strong initial fit | Strong fit |

| Poor current accuracy | Needed long term | Useful reset | Best fit |

| Continuous fulfillment | Strong fit | More disruptive | Strong fit |

6. Building a Reliable Cycle Counting Program

A cycle count program should operate as a control system rather than a recurring warehouse task. Therefore, every count needs a reason, schedule, owner, tolerance, investigation path, and review process.

6.1 Prioritize Inventory by Risk

ABC classification is a practical starting point. A products typically represent the highest financial or operational importance. B products receive moderate attention, while C products receive less frequent verification.

However, value alone is not enough. A low-cost component can stop production. Similarly, a modest accessory may be required to complete a high-value customer order.

Count priority should therefore consider:

- Financial value

- Transaction velocity

- Variance history

- Customer impact

- Production impact

- Shelf life

- Damage exposure

- Theft exposure

- Lot or serial requirements

- Supplier reliability

6.2 Set Cycle Count Frequency by Inventory Class

| Inventory group | Typical risk | Suggested starting frequency |

| A products | High value or operational importance | Weekly or monthly |

| B products | Moderate value and movement | Monthly or quarterly |

| C products | Lower value and slower movement | Quarterly or semiannually |

| High-variance products | Repeated discrepancies | More frequently |

| Expiring or regulated products | Compliance or spoilage risk | Based on policy and risk |

These frequencies are starting points. As accuracy improves, some products may need less attention. Conversely, products with repeated differences may need more frequent counting until the process issue is resolved.

Seasonality should also influence scheduling. For example, apparel companies may increase count frequency before a product launch, while food businesses may count expiring lots more often.

6.3 Use Blind Counts

A blind count hides the expected system quantity from the counter. As a result, the employee records what is physically present rather than attempting to match the system.

Blind counting reduces confirmation bias. However, it works only when products and locations can be identified clearly.

Therefore, the business should improve labels, barcode quality, bin identification, and item descriptions before depending heavily on blind counting.

6.4 Define Recount and Tolerance Rules

A recount should be required when the difference exceeds:

- A unit threshold

- A percentage threshold

- A financial-value limit

- A lot or serial mismatch

- A customer or production risk level

Furthermore, high-value or regulated inventory may require independent verification even when the unit variance is small.

Tolerance rules should reflect business risk. A one-unit variance may be immaterial for inexpensive packaging but highly significant for serialized equipment.

6.5 Separate Counting From Adjustment Approval

The same employee should not control every stage of a material inventory adjustment.

Instead, responsibilities should be separated across:

- Counting

- Recounting

- Variance investigation

- Adjustment approval

- Financial review

This separation improves accountability and reduces the risk of unexplained changes. Moreover, it gives finance and operations a consistent record of why inventory was adjusted.

6.6 Investigate Variances Before Posting Adjustments

When a difference appears, the team should review:

- Purchase receipts

- Putaway records

- Picks and shipments

- Warehouse transfers

- Returns

- Damage records

- Work orders

- Units of measure

- Manual adjustments

- Neighboring bins

Because cycle counts occur regularly, these transactions are usually recent enough to review.

Nevertheless, investigation should be proportional to risk. A small difference in low-value packaging may not require the same review as a missing serialized product.

6.7 Avoid Common Cycle Counting Mistakes

One common mistake is measuring only completion. A warehouse may complete every task while inventory accuracy remains weak.

Other mistakes include:

- Counting only easy products

- Displaying expected quantities

- Ignoring location accuracy

- Adjusting without investigation

- Failing to review repeated variances

- Allowing overdue tasks to accumulate

- Using the same frequency for every SKU

Ultimately, a successful program measures whether counting reduces future errors.

7. Planning and Executing a Physical Inventory Count

A successful physical count depends on preparation. Therefore, the warehouse should be organized before counters enter the aisles.

7.1 Define the Count Scope and Timing

First, determine whether the count covers the full company, one warehouse, selected products, or specific locations.

Next, choose a low-volume period. Whenever possible, avoid promotions, seasonal peaks, major inbound deliveries, and warehouse reorganizations.

The scope should also identify off-site inventory, consignment stock, third-party warehouses, returns, work in process, and goods waiting for quality inspection.

7.2 Prepare Warehouse Locations

Before the count:

- Clean and label bins

- Separate damaged stock

- Isolate quarantined inventory

- Resolve unidentified products

- Clear receiving areas

- Clear shipping stages

- Review open transfers

- Identify off-site inventory

- Confirm lots and serial numbers

As a result, counters spend less time interpreting warehouse conditions.

Preparation should begin well before count day. Otherwise, employees may discover mixed inventory, missing labels, and open transactions while counting is already underway.

7.3 Create Transaction Cutoff Rules

Receiving, shipping, transfers, returns, and production movements can invalidate a physical count.

A full freeze may not always be possible. Nevertheless, every movement during the count must follow a documented process. Otherwise, inventory may be counted twice or excluded entirely.

For example, an urgent shipment may be allowed during the count. However, the business must record whether the product was counted before or after it left the warehouse.

7.4 Assign Count Teams and Warehouse Zones

Divide the facility into clear zones. Assign primary counters, supervisors, and independent recount teams.

Additionally, provide instructions for:

- Sealed cartons

- Partial cases

- Mixed bins

- Kits

- Lots

- Serial numbers

- Staged shipments

- Work-in-process inventory

- Inventory outside normal locations

Count routes should prevent teams from skipping bins or counting the same location twice.

7.5 Reconcile and Approve Physical Count Differences

After employees complete the first count, compare the physical quantity with the system balance.

Significant differences should be recounted before adjustment. Furthermore, the business should retain:

- Original quantity

- Counted quantity

- Variance

- Financial value

- Reason code

- Counter

- Approver

- Posting date

This audit history helps finance understand how the final inventory value changed.

7.6 Review the Count After Completion

A physical count should produce an improvement plan.

Therefore, management should review:

- Total adjustment value

- Largest discrepancies

- Recount rates

- Unidentified stock

- Problem locations

- Repeated causes

- Process failures

- Corrective-action owners

Without this review, the same errors may return during the next count.

8. Inventory Variance, Reconciliation, and Accounting Control

Inventory differences affect more than available stock. They can also change purchasing, forecasting, production, inventory valuation, cost of goods sold, and gross margin.

8.1 Quantity Variance Versus Value Variance

A quantity variance measures missing or excess units. A value variance measures the financial effect.

For example, 50 missing low-cost components may have a smaller financial impact than one missing finished product. However, those components may still stop production. Therefore, businesses should measure both financial and operational significance.

A company should also separate location variance from total quantity variance. The total number of units may be correct, yet inventory may be stored in the wrong warehouse or bin.

8.2 Common Causes of Inventory Discrepancies

| Variance cause | Typical symptom | Investigation |

| Receiving error | System quantity exceeds physical stock | Review receipt and putaway |

| Picking error | Wrong quantity shipped | Review pick and shipment |

| Transfer error | One warehouse is short and another is over | Review transfer status |

| Unit conversion | Large proportional difference | Review unit settings |

| Unrecorded damage | Physical quantity is lower | Review damage records |

| Return error | Sellable and damaged stock disagree | Review return disposition |

| Production error | Components or output differ | Review work order activity |

8.3 How Inventory Adjustments Affect Accounting

An approved adjustment may affect:

- Inventory assets

- Cost of goods sold

- Shrink accounts

- Write-off accounts

- Production variances

- Gross margin

Therefore, finance should have visibility into the quantity, value, reason, approver, and posting date.

Additionally, adjustment reason codes should be specific enough to support analysis. A generic “inventory correction” code does not tell management whether the issue came from receiving, picking, returns, damage, or production.

8.4 Why Repeated Adjustments Require Process Correction

Repeated differences for the same product, bin, or transaction type signal a larger process issue.

For example, recurring shortages may result from poor pick confirmation. Meanwhile, repeated overages may indicate incomplete receiving or transfer transactions.

Consequently, management should not treat every adjustment as a successful correction. Instead, repeated variances should trigger training, process, label, integration, or system review.

9. Cycle Count vs Physical Count in ERP and WMS Workflows

The cycle count vs physical count process becomes easier to manage when inventory, warehouse, accounting, purchasing, and reporting workflows share the same data.

9.1 Automating Cycle Counts With Cloud ERP

A connected cloud ERP platform can organize count schedules, record differences, manage approvals, and update related inventory and financial records.

Xorosoft combines inventory management, accounting, purchasing, warehouse operations, manufacturing, forecasting, reporting, and ecommerce workflows. Therefore, it can support businesses where inventory discrepancies affect more than the warehouse.

For example, an approved adjustment can update inventory availability while also informing purchasing and finance. As a result, teams do not need to reconcile several disconnected applications.

9.2 Managing Warehouse Counts With WMS

A warehouse management system can direct employees to bins, support barcode scanning, hide expected quantities, trigger recounts, and measure accuracy by warehouse or location.

Additionally, Xorosoft can support multi-warehouse businesses where each facility follows a different schedule while management reviews consolidated accuracy and variance reporting.

A WMS can also help verify bin, lot, serial, and license-plate information. Therefore, teams can measure more than total quantity accuracy.

9.3 Connecting Inventory Adjustments With Accounting

An inventory adjustment can affect purchasing recommendations, available-to-sell inventory, inventory valuation, and gross margin.

A connected ERP for inventory-driven businesses can prevent the warehouse from treating quantity corrections as isolated activities. Instead, inventory, accounting, purchasing, manufacturing, and forecasting teams work from connected records.

Moreover, integrated workflows can reduce duplicate data entry and shorten reconciliation. Finance can review the financial effect without waiting for a separate spreadsheet from the warehouse.

9.4 Recognizing When Basic Inventory Tools Have Reached Their Limit

A business may have outgrown spreadsheets or inventory-only applications when it manages:

- Multiple warehouses

- Large SKU catalogs

- Frequent adjustments

- Separate inventory and accounting records

- Shopify and Amazon operations

- Wholesale and EDI orders

- Lot or serial tracking

- Manufacturing workflows

- Slow month-end reconciliation

At that stage, teams may compare NetSuite, Acumatica, Cin7, Brightpearl, Fishbowl, Sage, Business Central, and other systems. A neutral Xorosoft vs NetSuite comparison can help businesses evaluate implementation approach, complexity, and operational fit.

9.5 Comparing Inventory Counting Software

| Capability | Spreadsheet | Inventory app | WMS | Connected ERP and WMS |

| Scheduled counts | Limited | Sometimes | Yes | Yes |

| Barcode scanning | Limited | Often | Yes | Yes |

| Multi-warehouse support | Difficult | Varies | Yes | Yes |

| Lot and serial tracking | Difficult | Varies | Yes | Yes |

| Approval workflows | Manual | Varies | Often | Yes |

| Accounting integration | No | Limited | Limited | Yes |

| Purchasing impact | Manual | Limited | Limited | Connected |

| Financial reporting | No | Limited | Limited | Connected |

10. Cycle Count vs Physical Count by Industry

The best cycle count vs physical count approach changes by industry because inventory risk differs across apparel, wholesale, furniture, food, ecommerce, and manufacturing.

10.1 Apparel and Fashion Inventory

Apparel businesses manage style, size, color, season, channel, and warehouse combinations. Similar products can easily be placed in the wrong bin.

Therefore, cycle counting should prioritize:

- New collections

- High-return products

- Fast-moving sizes

- Similar variants

- Seasonal products

- High-value items

A full physical count may still be useful before major seasonal changes or system migrations.

Xorosoft supports inventory-driven industries including apparel, wholesale distribution, furniture, sporting goods, food, and manufacturing.

10.2 Wholesale Distribution Inventory

Wholesale distributors may manage high order volume, customer allocations, case and each units, EDI transactions, and multiple warehouses.

As a result, a hybrid policy is often practical. Cycle counts maintain daily control, while broader physical counts validate high-risk facilities and period-end balances.

Customer-specific pricing and allocation rules also increase the cost of inaccurate inventory. Therefore, distributors need timely verification rather than a single annual correction.

10.3 Furniture and Sporting Goods

Furniture and sporting goods companies may store bulky, high-value, serialized, or location-sensitive products across racks, floors, showrooms, and overflow spaces.

Consequently, the count should verify both quantity and location. Serialized or high-value products may also require independent recounts.

A full physical count may be especially useful after a showroom reset or warehouse reconfiguration.

10.4 Food and Beverage Inventory

Food businesses may need to verify quantity, lot, expiration date, storage status, and production stage.

Moreover, waste, spoilage, samples, and quality holds require controlled adjustments. Therefore, count frequency should reflect shelf life and traceability risk.

In addition, inventory accuracy should include lot and expiration accuracy, not only total quantity.

10.5 Manufacturing Inventory

Manufacturers count raw materials, components, work in process, subassemblies, and finished goods.

Differences may arise when consumption, scrap, output, or backflushing does not match physical activity. Consequently, cycle counting should work alongside BOM control, work orders, and production reporting.

Low-cost components may deserve frequent counts when shortages can stop production. Therefore, value-based ABC classification should be supplemented with operational risk.

10.6 Shopify and Amazon Inventory Reconciliation

Multi-channel sellers need accurate quantities across storefronts, marketplaces, warehouses, and third-party fulfillment locations.

Returns, cancellations, bundles, and synchronization delays can create additional discrepancies. Therefore, Xorosoft can act as the operational system behind Shopify by connecting inventory, purchasing, accounting, warehouse operations, and forecasting.

Shopify merchants can review the Xorosoft ERP app for Shopify when inventory requirements extend beyond storefront-level quantity management.

11. Inventory Counting KPIs That Reveal Process Quality

Count completion alone does not prove inventory accuracy. Therefore, teams should monitor both activity and results.

11.1 Inventory Record Accuracy

A common formula is:

Accurate inventory records ÷ Total records counted × 100

However, the company must define what “accurate” means. Some businesses require an exact match, while others permit an approved tolerance.

The calculation should also specify whether accuracy is measured by SKU, bin, location, lot, serial number, or total quantity.

11.2 Unit and Value Variance

Track both units and financial value. Otherwise, many low-value differences may distract management from a small number of financially significant problems.

Additionally, review operational impact. A low-value component may have a high production consequence.

11.3 Recount Rate

A high recount rate may reveal:

- Unclear instructions

- Poor labels

- Mixed bins

- Difficult units of measure

- Weak first-count discipline

Therefore, recount rate should be reviewed by warehouse, product class, and employee team.

11.4 Adjustment Frequency

Measure how often the same product, location, warehouse, or transaction type requires adjustment.

Repeated adjustments indicate that corrective action is incomplete. Consequently, high-frequency adjustment patterns should receive management attention.

11.5 Cycle Count Completion Rate

Completion shows whether scheduled work occurred. Nevertheless, it should always be reviewed beside accuracy, variance value, and overdue counts.

A warehouse that completes every count but continues generating large variances is not improving.

11.6 Root-Cause Resolution Rate

Track whether identified issues received corrective action. For example, a completed investigation without an owner or deadline does not improve inventory control.

Moreover, management should review whether the issue returned after corrective action.

11.7 Accuracy by Warehouse and Product Class

A company-wide average may hide a weak warehouse. Therefore, compare results by:

- Warehouse

- SKU class

- Product family

- Bin type

- Shift

- Transaction process

This analysis helps leadership focus on the locations and workflows creating the greatest risk.

12. Frequently Asked Questions About Inventory Counting

12.1 What Is Cycle Counting?

Cycle counting is the recurring verification of selected inventory. Businesses may count products by value, movement, risk, or discrepancy history. Afterward, the physical result is compared with the system quantity, and material differences are investigated.

12.2 What Is a Physical Inventory Count?

A physical inventory count verifies all inventory within a defined scope at one point in time. The scope may include an entire company, warehouse, store, or selected product category.

12.3 What Is the Difference Between Cycle Counting and Physical Counting?

In a cycle count vs physical count comparison, cycle counting verifies selected inventory throughout the year, while a physical count verifies the full defined scope during one event. Therefore, cycle counting supports continuous control, whereas physical counting provides complete point-in-time validation.

12.4 Is Cycle Counting a Type of Physical Inventory?

Yes. Employees physically verify stock during both methods. However, cycle counting covers selected products or locations on a recurring schedule.

12.5 Is Cycle Counting Better Than a Physical Count?

The answer depends on the business. In the cycle count vs physical count decision, cycle counting generally fits active and complex operations, while physical counting may be more appropriate for smaller inventories, system changes, or full period-end verification.

12.6 Can Cycle Counting Replace Annual Physical Inventory?

A mature cycle count program may reduce dependence on annual counts. Nevertheless, auditors, lenders, accounting policies, or company governance may still require full verification.

12.7 How Often Should Cycle Counts Be Performed?

Frequency should reflect value, transaction volume, discrepancy history, shelf life, customer impact, and compliance risk. High-priority inventory may be counted weekly or monthly, while stable products may be counted quarterly.

12.8 How Often Should a Physical Inventory Count Be Performed?

The schedule depends on accounting requirements, inventory risk, and the reliability of ongoing controls. Some businesses count annually, whereas others perform full counts only after major operational changes.

12.9 What Is ABC Cycle Counting?

ABC cycle counting groups inventory by importance. A products receive the highest count frequency, B products receive moderate attention, and C products receive less frequent counting.

12.10 Which Inventory Should Be Counted Most Frequently?

High-value, fast-moving, regulated, expiring, serialized, frequently adjusted, or customer-critical inventory should be counted most frequently.

12.11 What Is a Blind Inventory Count?

A blind count hides the system quantity from the employee. Therefore, the counter records what is physically present without being influenced by the expected balance.

12.12 Should Warehouse Activity Stop During a Cycle Count?

Usually, the full warehouse does not need to stop. However, activity affecting the selected products or locations must be prevented or tightly controlled.

12.13 Should Warehouse Activity Stop During a Physical Count?

A transaction freeze is often preferred. Nevertheless, when operations must continue, every movement should follow a documented control process.

12.14 Who Should Perform Inventory Counts?

Trained warehouse employees, inventory-control specialists, supervisors, or independent count teams may perform counts. Material differences should receive separate review.

12.15 When Should a Recount Be Required?

Require a recount when the variance exceeds unit, percentage, or financial thresholds. Additionally, high-value or regulated inventory may require independent verification.

12.16 How Is Cycle Count Accuracy Calculated?

Divide accurate records by total records counted and multiply by 100. Businesses may also measure accuracy by units, value, bin, lot, or serial number.

12.17 What Is an Acceptable Inventory Accuracy Rate?

The target depends on industry, risk, and measurement method. Therefore, high-value, regulated, expiring, serialized, or production-critical inventory may require stricter standards.

12.18 What Causes Cycle Count Discrepancies?

Common causes include receiving errors, incorrect putaway, unconfirmed picks, transfer timing, returns, damage, theft, unit conversions, and production consumption.

12.19 How Should Inventory Variances Be Investigated?

Review receipts, shipments, transfers, returns, work orders, damage records, adjustments, neighboring bins, units of measure, lots, and serial numbers.

12.20 Can Barcode Scanners Improve Inventory Counting?

Yes. Barcode scanners reduce identification and entry errors. However, they cannot correct poor labels, inaccurate item data, or weak procedures.

12.21 How Does a WMS Support Cycle Counting?

A WMS can schedule tasks, direct counters to bins, support barcode scanning, hide expected quantities, trigger recounts, and report results by location.

12.22 How Does ERP Connect Counts With Accounting?

ERP can post approved adjustments to inventory and financial records through one controlled transaction. Moreover, it can update purchasing, valuation, production, and reporting.

12.23 Can Cycle Counting Work Across Multiple Warehouses?

Yes. Each warehouse can follow a schedule based on volume, risk, and accuracy. Meanwhile, central reporting can compare results across the network.

12.24 When Should a Business Upgrade From Spreadsheets?

An upgrade becomes relevant when the company manages multiple warehouses, large SKU catalogs, ecommerce, wholesale, EDI, manufacturing, lots, serials, or frequent adjustments.

12.25 Should Small Businesses Use Cycle Counting?

Small businesses can benefit when their inventory is operationally complex. For example, a company with many variants, frequent returns, or multiple locations may need cycle counting even with modest revenue.

13. Final Takeaway: Build a Counting Policy That Prevents Repeat Errors

The final cycle count vs physical count decision should reflect inventory risk, operational complexity, and how quickly discrepancies need to be identified.

Use cycle counting when continuous fulfillment, multiple warehouses, large SKU catalogs, and frequent transactions make ongoing verification necessary. In contrast, use a physical count when the business needs a complete reset, a reliable starting balance, or broad period-end validation.

In many cases, however, a hybrid approach provides the strongest control. Cycle counting maintains accuracy throughout the year, while physical counts provide broader validation when required.

Nevertheless, counting frequency is only one part of inventory accuracy. Reliable records also depend on disciplined receiving, correct putaway, confirmed picking, controlled transfers, clear return disposition, accurate production reporting, and approved adjustments.

As complexity grows, the cycle count vs physical count process must connect with purchasing, accounting, forecasting, warehouse management, manufacturing, ecommerce, and reporting. Otherwise, the warehouse may correct quantities while other teams continue using disconnected or outdated information.

Businesses evaluating a more controlled inventory environment can book a personalized Xorosoft demo to review their warehouse structure, counting process, Shopify or Amazon operations, EDI requirements, purchasing workflows, manufacturing needs, and accounting reconciliation.